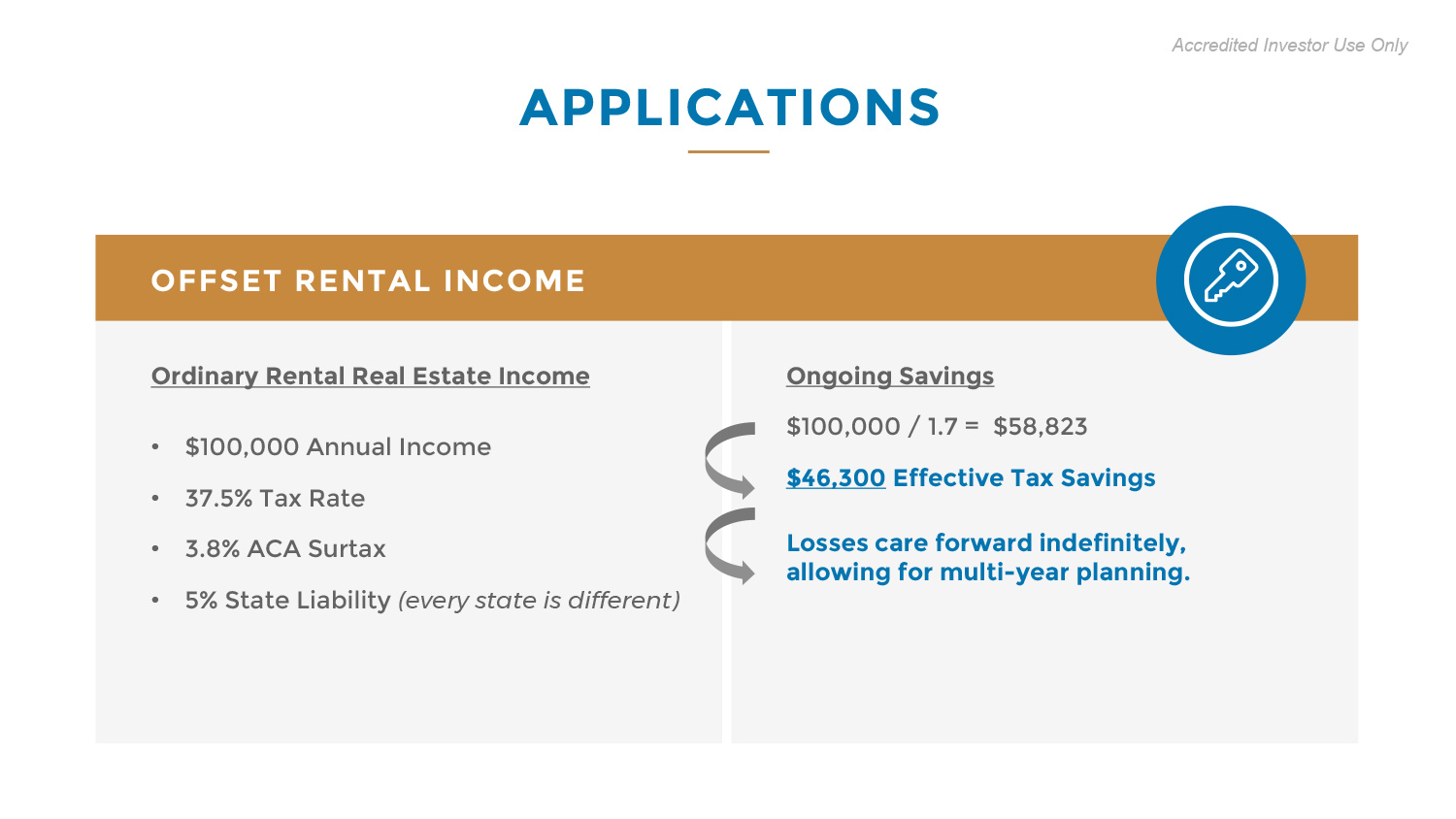

While real estate is typically viewed as an appreciating asset in the eyes of investors, from a tax perspective, the components of the building are depreciating assets that are eligible for tax write-offs over their useful life.

Accelerated or bonus depreciation allows businesses to deduct a large percentage of the cost of eligible purchases the year they acquire them, rather than depreciating them over a period of years.

The write-off can be taken against active or passive income.

The 2017 Tax Cuts and Jobs Act increased the amount of bonus depreciation and expanded the types of property that qualify.

By completing a cost segregation study we plan to utilize accelerated depreciation in all our acquisitions.

We plan to take the maximum allowable bonus depreciation on qualifying properties in the first year a property is placed into service.

Because the fund is taxed as a partnership for federal income tax purposes, any deductions taken in respect of bonus depreciation will pass-through to its members.