Deferring Taxes on Sale of Business

Long-Term Wealth Preservation through Strategic Opportunity Zone Allocation

The Qualified Opportunity Zone Program, created by the Tax Cuts and Jobs Act of 2017, is a tax incentive program designed to encourage long-term private sector investments in designated communities known as Qualified Opportunity Zones by delivering certain tax benefits to investors through investment vehicles called Qualified Opportunity Funds.

A designated census tract in the United States that has been selected by a state governor and certified by the U.S. Department of Treasury for inclusion in the QOZ Program. There are over 8,700 Qualified Opportunity Zones.

An investment vehicle organized as either a partnership or corporation that holds at least 90% of its assets in QOZ property. QOFs can make investments in a wide variety of real estate or new or existing businesses, including commercial real estate, housing, infrastructure and start-up businesses. QOFs can hold single or multiple assets.

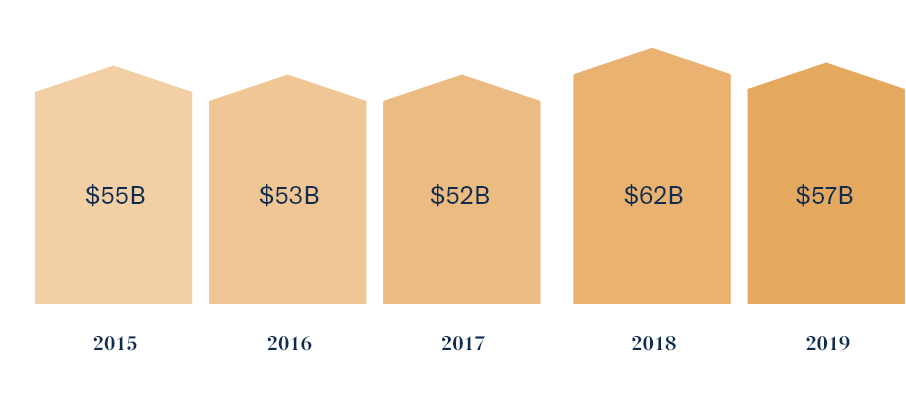

Total investments in markets now deemed Qualified Opportunity Zones. Even before the current legislation was enacted, these areas attracted significant institutional capital.

Newmark Knight Frank Research, Real Capital Analytics (inclusive of activity in areas prior to designation).

the inclusion of capital gains invested in a Qualified Opportunity Fund as taxable income until 2026

the taxable capital gain amount through step-up in basis by:

10% if held at least 5 years prior to Dec. 31, 2026. 15% if held at least 7 years prior to Dec. 31, 2026

on the appreciation of your investment in the Qualified Opportunity Fund if held at least 10 years

Created in 2017, as part of the Tax Cuts and Jobs Act, QOZs help stimulate economic growth in overlooked communities across the country. To achieve this, Congress passed special tax incentives to encourage investors to recognize a capital gain from the sale of an asset which they otherwise may not have sold due to the tax liability.

Under certain requirements, investors can roll over a portion, or all their capital gains into a Qualified Opportunity Zone Fund (QOF)—This gives them the potential ability to defer, or to avoid taxes entirely. This is a win-win program with benefits for multiple parties. Investors receive tax incentives to keep more of their capital gains, and afflicted communities in the U.S. receive the resources needed to turn their economy around. With 8700 QOZs located around the country, now is the time for investors to investigate these programs.

A unique initiative that preserves capital gains and delivers potential tax benefits to investors.

Created by the Tax Cuts and Jobs Act of 2017.

8762 Qualified Opportunity Zones located across the U.S.

Encourages long-term investments in designated communities known as Qualified Opportunity Zones.

Individuals or entities that invest their capital gains in these communities through investment vehicles called Qualified Opportunity Funds may receive multiple tax benefits.

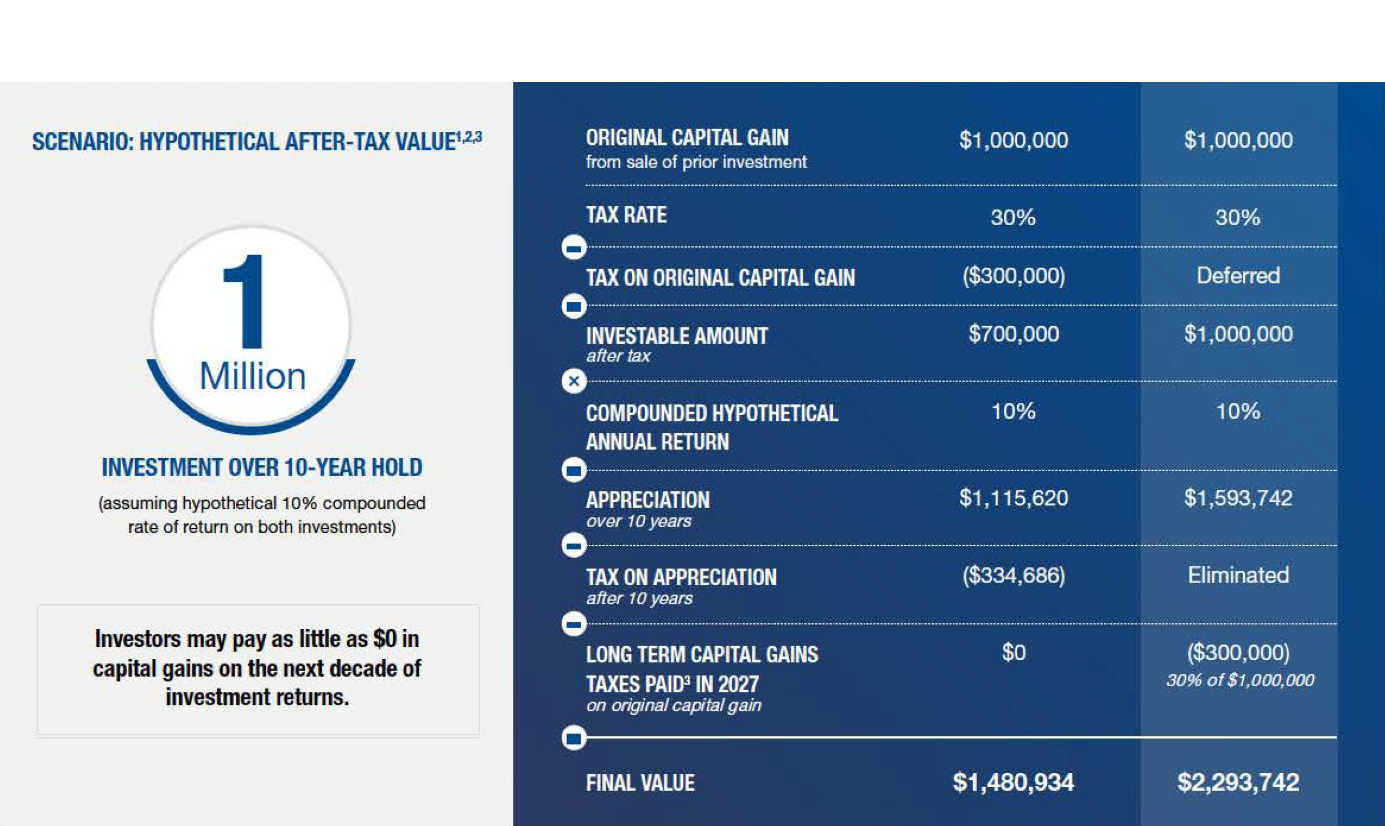

Below is a chart that shows the difference in returns on two hypothetical investments with the same internal rate of return (IRR}:

1. ThIs illustration assumes the investor is subject to the top marginal u_s_ federal income tax rate of 20% on long-term capital gains for individuals, the net investment income tax of 3.8%

and a state tax of 6.2% for a total tax liability of 30%. No brokerage or investment advisory fees are accounted for with respect to the non-OOF example above.

2. This assumes that the OOF investor is a resident of a state that conforms with the OOZ Program.

3. Assumes that the investor has no capital losses to reduce such capital gain and refers to the inclusion of the original, invested capital gains in such investor’s taxable income on December 31, 2026.

QOFs and 1031 exchanges both offer the potential for significant tax incentives and can be used in conjunction with one another. However, the two investment vehicles have many differences, and therefore, may be appropriate for different investors.

Gains recognized from the disposition of the following assets are eligible to receive the respective tax benefits of the 1031 exchanges and investments in QOFs.

We don’t just offer advice; we architect solutions. Explore our real-world case studies to see how we navigate complex tax laws and market volatility to protect and grow our clients’ wealth.

Long-Term Wealth Preservation through Strategic Opportunity Zone Allocation