DST Diversification

Attempting to reduce risk in real estate real estate investments is possible by practicing diversification. Instead of investing in a single property with concentration risk, prudence dictates investing in a number of properties with different investment and risk parameters.

By investing in different asset classes, different locations and properties leased by different tenants, you may be able to mitigate certain risks associated with investing in a concentrated investment. By diversifying your holding periods, all of your investments will not mature and have to be sold at the same time. If you invest in Delaware Statutory Trusts, it also is practical to diversify by sponsorship so that your assets are not all managed by the same real estate firm.

DST IN ACTION

A sample six-property diversified DST portfolio is shown below. This illustrates investment in a more diversified portfolio of DST replacement properties that could qualify for tax deferral under Section 1031.

A diversified portfolio such as this would not be possible with “whole” properties for an exchanger with only $1 million of equity. More exchangers can diversify by using DSTs to acquire interests in investment-grade properties, it’s possible for a larger number of exchangers to diversify. In this way, DSTs can be used to reduce investment risk.

IN CONCLUSION

Bottom Line: Investors who own a more diversified portfolio enjoy reduced risk, especially during challenging economic times, when compared with investors in a single asset. Section 1031 exchangers acquiring replacement property should diversify to reduce risk. In this way, you can seek to both qualify for tax deferral and reduce the inherent risk of making new real estate investments.

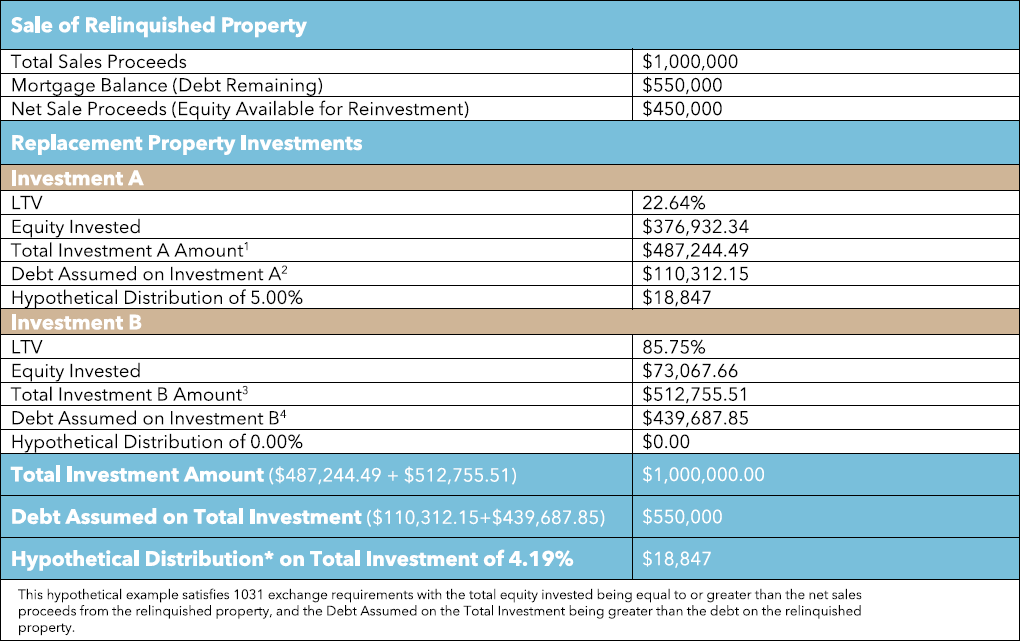

Potential Solution to Cover 1031 Exchange Debt Requirements

Investors can blend a combination of a highly leveraged property and a cash flow property to exactly meet the debt, equity, and overall requirements of the exchange without having to come up with additional equity. Investors can use a Zero to inexpensively meet the debt requirements of an exchange so that no additional equity is required to meet the overall value requirement.

Highly leveraged, zero cash flow properties (Zeros) are investment structures that help investors easily meet the debt and equity requirements of a 1031 Exchange. These properties have debt service obligations equal to (or nearly equal to) the net operating income of the property. This highly leveraged solution is possible because of the investment grade credit of the tenant and the absolute triple net nature of their long-term leases.

Example: An investor has sold a property for $1,000,000 and would like to do a 1031 Exchange. The Relinquished Property was moderately leveraged netting the seller $450,000 equity for reinvestment. To fulfill the debt requirement of the 1031 Exchange and complete the exchange, the sum of the cash invested, and the debt placed on the Replacement Property must be equal to or greater than the sum of the net cash proceeds, and the debt that was on the Relinquished Property. To meet their need, the investor may choose two Replacement Property investments to complete their Exchange. One with a lower loan -to-value ratio (LTV), the second with a high loan-to-value (LTV). Below, is how a Zero could be utilized to meet this investor’s Exchange Requirement.

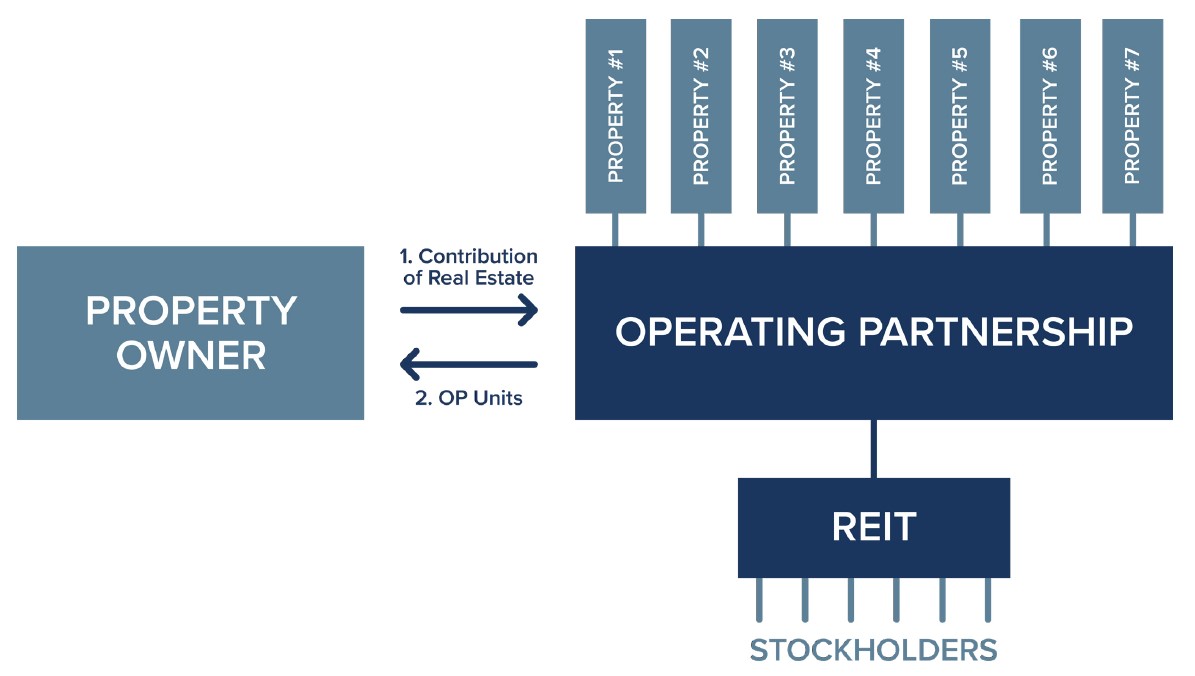

INTRODUCTION TO REITS AND OPERATING PARTNERSHIPS

Real estate investment trusts (REITs) typically own their real estate in an operating partnership known as an OP. The OP is structured as a partnership to obtain favorable tax treatment under the Internal Revenue Code. Section 721 of the Code provides favorable treatment for owners who exchange their real estate for OP units. This is commonly referred to as a 721 exchange, OP transaction or UPREIT.

OP Unit holders receive a share of cash flow from each of the properties in the OP. They typically receive the same rate of return on their equity as REIT stockholders receive on their stock.

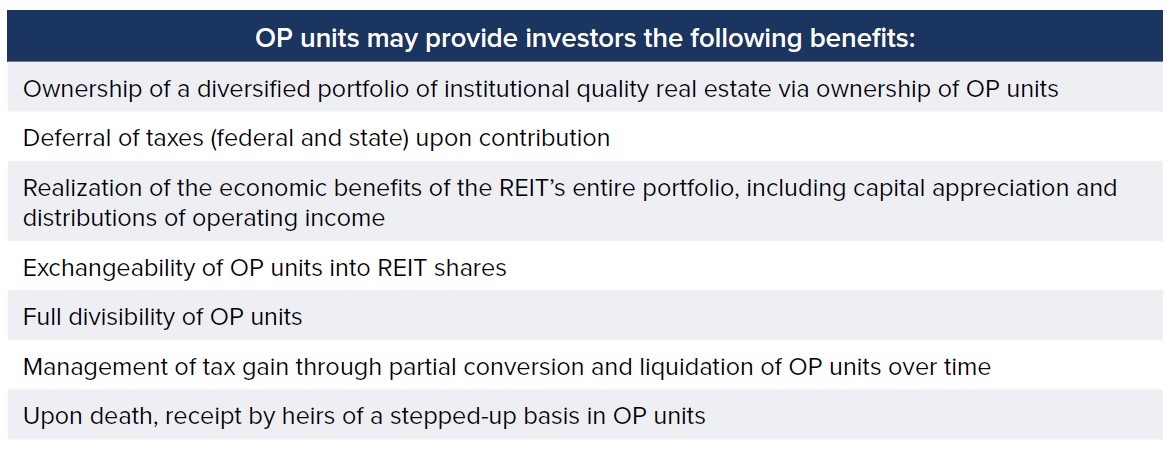

Summarized below are numerous benefits to owners who enter into OP transactions, including the reduction of risk by diversifying compared to ownership of a single property. Also, OP distributions are protected compared to ownership of a single property because the OP owns a large portfolio of properties.

WHAT IS A 721 EXCHANGE/OP TRANSACTION?

In a Section 721 exchange, the owner exchanges real estate for OP units of a REIT. Instead of receiving cash in a taxable transaction, the owner receives OP units. Unlike a taxable sale, the gain is deferred under Section 721.

Section 721 is similar to Section 1031 governing like-kind exchanges, another popular method of deferring gain on the sale of investment real estate. Section 721 exchanges have become a popular strategy among real estate owners looking for diversification and other benefits described below.

TAX BENEFITS OF SECTION 721

Section 721 defers taxation for owners of real estate who contribute their property to an OP. The gain that would be recognized in a taxable sale is deferred. The gain is deferred until the owner elects to sell the OP units in a taxable transaction. The owner has the ability to hold OP units indefinitely or time the sale to coincide with tax or financial planning strategies.

The tax deferral becomes permanent (the tax is essentially forgiven) upon death. The heirs, upon death of the OP holder, receive a stepped-up tax basis in the OP units (tax basis equal to fair market value). This means that the heirs can then sell free of taxes (federal and state). In this way, the deferral becomes permanent upon death.

Section 721 is a popular alternative to a taxable sale for real estate owners interested in a taxfavored investment with an institutional partner.

OP/UPREIT STRUCTURE

A 721 transaction allows an investor to exchange real property for operating partnership units, which may then be converted into REIT shares and sold.

BENEFITS OF SECTION 721 EXCHANGES/OP TRANSACTIONS

Owners of real property enjoy numerous benefits from a 721 exchange:

1. No Taxable Gain. The gain that would be recognized in a taxable sale is deferred under Section 721. The gain is deferred until the holder of OP units elects to sell in a taxable transaction. The gain will be forgiven upon death of the holder.

2. Diversification. Owners who exchange real estate for OP units have the safety net of a more diversified investment because the OP owns a large portfolio of

properties. Owners can reduce their risk by diversifying in this manner compared to ownership of a single property. Also, the OP’s portfolio of properties helps

protect owners’ distributions of cash flow

3. Liquidity. REITs typically provide a liquidity option that is not available in a direct real estate investment. OP units may be exchanged for REIT shares and, then, sold on the market to create liquidity for some or all of the investment. Liquidity in this manner is not available to direct owners of real estate.

4. Estate and Tax Planning. OP units are conducive to estate and tax planning because they can be divided among the partners of a partnership or members

of a family. The divisibility of OP units permits some to hold and others to sell. This flexibility permits individualized tax and financial planning.

5. Passive Investment. Owners are able to convert actively managed real estate into a passive investment where a professionally managed, institutional REIT provides turn-key management and accounting services.

6. Transparency. REITs provide a high level of transparency and oversight by an independent board of directors.

These benefits can be obtained in a 721 exchange without triggering taxable gain (federal or state).

Target Property

For an OP transaction to be a viable strategy, the target property must meet the REIT’s investment criteria. REITs typically acquire investment grade properties and also interests in such properties, for example, DST interests.

HOW IT WORKS

The process is simple. The property owner and the REIT mutually agree on the fair market value for the property. The purchase price is typically determined by independent third-party appraisals.

Debt secured by the real estate will be assumed by the OP or repaid at closing. The owner will be released from all liability on their loan.

The real estate owner receives OP units with a value equal to 100% of their equity in the property (fair market value of the property less any debt assumed by the OP).

THE 721 ADVANTAGE

A Section 721 exchange offers many potential benefits, including:

LIQUIDTY OPTION — EXCHANGE OP UNITS FOR REIT SHARES

REITs typically provide liquidity via an option to exchange OP units for REIT shares that can be sold on the market. To obtain liquidity, the owner would exchange OP units for REIT shares, and then sell shares on the market.

The holder of OP units chooses when and how much of the OP units to sell. The decision to sell is made solely by the holder of OP units. This is a taxable transaction but provides liquidity not otherwise available in a direct real estate investment.

Best Candidates

Sellers of commercial real estate who face a large capital gains tax.

Candidates include: owners of appreciated real estate, long-time owners who have taken depreciation expenses over the years, and owners who have carried in a low tax basis from a previous exchange.

In general, two factors that contribute to a large capital gain are appreciation of the property and depreciation taken over time, which lowers the owner’s tax basis.

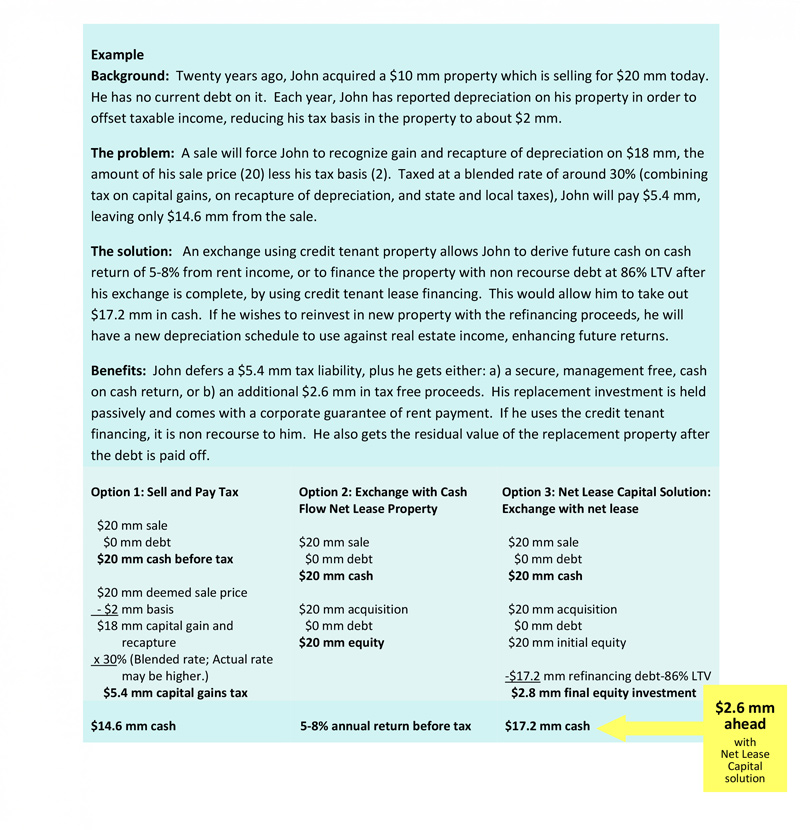

The Problem

Capital gains tax may reduce the seller’s cash proceeds or prevent the seller from selling at all. A 1031 exchange for typical property can defer the tax, but, if the tax basis is low, provides suboptimal outcomes for four reasons:

1) Proceeds are not maximized; sale proceeds are locked up;

2) Little depreciation remains to offset income, since the low tax basis from the sale property is carried into the exchange property. After-tax yields are significantly lower;

3) Risk of failure is high due to strict 1031 timing requirements;

4 ) In instances where owners have lost equity in their properties, more equity is needed to buy replacement property of equal value in order to complete a 1031 exchange, with owners having to come out of pocket.

The Solution

Complete a 1031 exchange using a replacement property net leased for a long term to an investment grade credit tenant.

The liquidity and availability of net lease properties provides certainty in meeting 1031 deadlines, even under tight timeframes.

The property owner may derive significantly more cash from the transaction by refinancing after the exchange is complete, using credit based financing that reaches 86% LTV while mitigating phantom income. By using financing proceeds to make future acquisitions, new property will be acquired at full tax basis so that a full depreciation schedule is available to offset income, enhancing yield.

Traits of the net lease property which help make this solution compelling include:

Breakwater Capital provides property, financing and transaction structures to optimize financial outcomes.

The properties used are management free with investment grade credit tenants on long term leases. Transaction structures eliminate ongoing tax concerns, decrease valuation volatility, and offer easy exit strategies. Breakwater Capital is the nation’s leading expert in this type of transaction, with over $14 billion of transactions closed.